Just as everyone has long expected, the EPF is finally beating the war drum of upping the withdrawal age, in trying to be logical and in trying to be in lockstep with the retirement age. This will of course deny millions of contributors of early access to their hard-earned money. To avoid huge public backlash, the EPF decided to perform a “market survey” first, just to have a taste what the public is actually thinking. Ever since the government pushed the retirement age upward to 60 years old, the threat of higher withdrawal age is always looming large for all Malaysians.

Just as everyone has long expected, the EPF is finally beating the war drum of upping the withdrawal age, in trying to be logical and in trying to be in lockstep with the retirement age. This will of course deny millions of contributors of early access to their hard-earned money. To avoid huge public backlash, the EPF decided to perform a “market survey” first, just to have a taste what the public is actually thinking. Ever since the government pushed the retirement age upward to 60 years old, the threat of higher withdrawal age is always looming large for all Malaysians.

In order to support the horrendous beating main drum, the EPF “disclosed” some data to “scare” Malaysians into giving away their birthright to their really hard-earned money, tucked away so safely by the EPF. The EPF repeatedly gave away one sided facts, without really disclosing the entire data in question. This has been a big problem for the EPF. I and so many others out there, are truly skeptical. Retirees running out of money? Where are they by the way? And why did they ran out of money? If RM126,000 isn’t enough for them, will RM156,000 be enough? Was the problem is really of inadequate savings, or was there something much more to it? Sometimes, even a million ringgit will not be enough for a fool, yet, if a fool want to part with his money, who are we to stop the person from doing that? Our best bet is always through better education, never through ridiculous government control over the people [I do consider the EPF to be part of the government].

Consider this simple example, not from the EPF to the public, but from a minister during a question session in parliament (The Star, Nov 20, 2014).

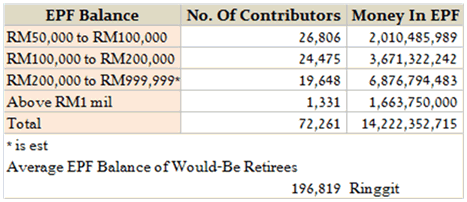

69% of would be retirees have less than RM50,000 in their EPF accounts.

Another 26,898 contributors or 11.5% have between RM50,001 and RM100,000 while 10.5% or 24,552 people have savings between RM100,001 and RM200,000 in their account according to the minister during question time in the Dewan Rakyat.

Well, if this number is absolutely true and reflective of all workers, then Malaysia will be in big trouble. But alas, it is not to be. Never mind the missing 10% that was forgotten to be included in the statistics above (it doesn’t add to 100%), there is just no retirement crisis looming in Malaysia other than an imaginary one. Just how misleading the statistic revealed by the EPF/minister in order to scare the gullible public? In order to have only RM50,000 in the EPF upon retirement, one must work for JUST 11 months out of his or her entire working life! [Just three years for those earning the minimum salary]. Do remember that all deposits made into the EPF will be compounded for 30 years or more! It is clear that most of the 69% of the would-be retirees due for retirement are not even regular workers. They could be some housewives who stopped working a long time ago, and now living with a rich (really rich) husband and have many successful offspring, or they could be those who are now successful businessmen who quit their salaried jobs, created their own business, and are now millionaires many times over. Whatever the facts and whatever the reasons are, one thing is very clear; these 69%ters do not represent the regular and the typical Malaysian workers out there.

So if we exclude the 69% from the equation, what shall we have? Well according to the minister’s data, we will have just 37% of the retirees having between RM50,000 and RM100,000. The majority of them, will have more than RM100,000, and some (about 2%), have more than a million! This clearly is not warranting a crisis response from the public, especially so for the EPF.

I have calculated that the average EPF savings (from the miniscule amount of haphazard data available) for these would be retirees, is actually RM196,000 a person. This is much more than enough for a typical retirement expenses, until death.

My calculation matched the scant data available buried deep in the EPF website, which confirmed that for active contributors, their average savings a year before turning 55 is RM180,000. Never mind that back in 2008, those who were a year away from retirement has on average, only RM132,000 (total compounded increase of 36% in 2014). Without doing anything, without interference and without changing any of the EPF rules, why would a new group of would be retirees, have 36% more in their EPF compared to a same group, several years their senior? It is clear that retirees are doing better on their own, so let’s not disturb then at this moment in time (even with inflation included, the would-be retirees will end up with much more money than their predecessors). The EPF, as it is, is already a hugely successful retirement fund and no other tweak would be necessary. The 1,331 millionaires retiring in 2015 is already more than 10% of the entire millionaires in Malaysia (data based on Credit Suisse). I see no point in us creating ever more EPF millionaires to skew the statistics further just to please some people out there with a skewed agenda based on skewed data.

The data revealing that “69% of would-be retirees” have just RM50,000 or less in their EPF is so illogical for Malaysia’s regular workers, the following examples will illustrate just how crazy and how low it is.

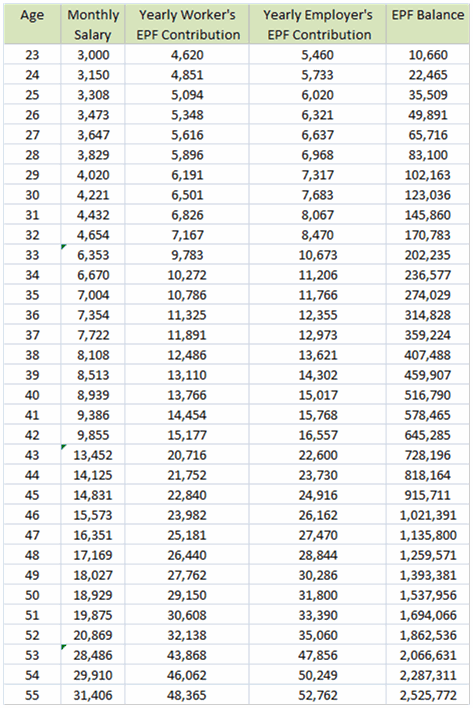

Situation 1 – The Typical

Note: Worker on an average salary of a typical Malaysian, having a regular salary increment of 5% a year, coupled with occasional promotions, yearly bonus included and EPF yearly dividends of 5.75%.

Easily, a person with a good career, with a normal starting salary, will be able to amass more than 2.1 million in the EPF upon retirement. Of course it will be less, as some may take the money out to invest into their property, which may grow as well. Regardless, the net effect would be the same. No crisis for a regular earning employee, and no adjustment of the rules by the EPF will be needed.

Assuming the employee takes out all of the money possible every time from Account 2 of the EPF, he will still ends up retiring with more than RM1.7 million in his Account 1. Crisis? Far from it. In fact, it could be a crisis of too much saved for retirement!

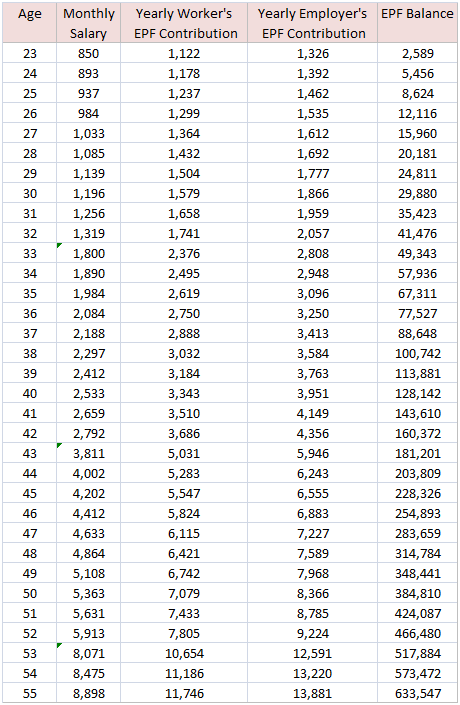

Situation 2 – The Poor & Uneducated

What if someone starts working at the minimum salary?

Note: Worker on minimum salary, started to work pretty late, salary increase is 5% a year, promotion every 10 years, no bonus paid at all and EPF dividend rate of 5.75% a year

Yes, he will retire comfortably; I see no problem at all. After working for more than 30 years, a person who started earning minimum wage with quite a ‘normal’ career increment would amassed RM633,547 by retirement age. In inflation corrected terms, in today’s money, he will be retiring with RM291,000. This is much more than comfortable. He would be able to achieve his dreams! Thanks EPF!

So how little must you save in order to retire with less than RM50,000? Let’s try a new situation, however illogical, where someone just continue to work and collecting only the minimum salary, devoid of any increment whatsoever for his entire lives!

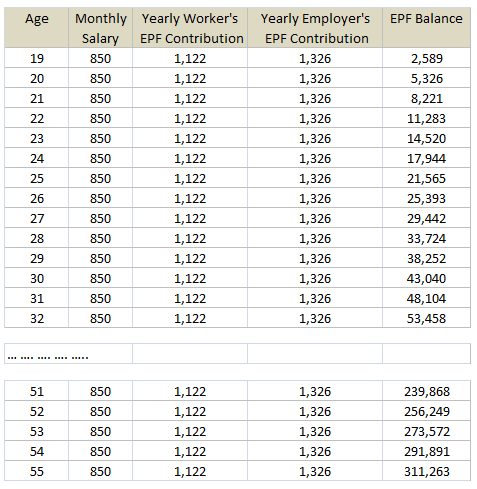

Situation 3 – The Forever Low Salary

Note: Forever on the minimum salary, started to work early, no salary increment whatsoever due to nasty bosses, no promotion whatsoever and certainly no bonus too! EPF yearly dividend is 5.75%

He will still retire rich. So even at minimum salary of RM850 a month, someone will easily be able to retire with RM311,000 in the EPF. What crisis??

So just how low must we go in order to retire without having enough in the EPF? Try this, don’t save at all in the EPF, other than the freely given BR1M money!

Situation 4 – The BR1M Collector

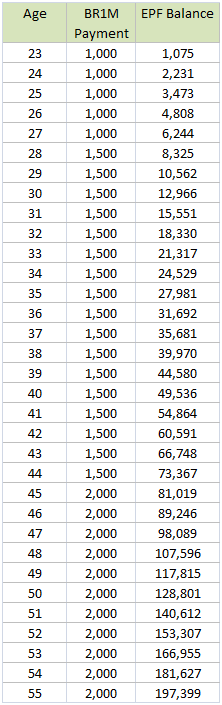

Nobody will believe it, but if you just collect BR1M and simply save the RM1,000 into the EPF every year, once a year, you will still end up with too much money!

Note: Too lazy to work, hanging out all day long, drinking and smoking, collects the BR1M payments and deposit it into the EPF

Yes, you will end up with RM197,000 upon turning 55, without really needing to work and to save! If those on BR1M can do it, so can you and anyone else! Nobody will not have enough in their EPF, everyone would have too much!

It is so easy to save for retirement, one just have to contribute the minimal amount, and they would be set. EPF argument just don’t cut it, especially without releasing the necessary data to back it. For those who are always complaining that they don’t or won’t have enough upon retirement, but still have money to burn by buying cigarettes, just consider this:

Stop smoking! You will end up with RM459,000 extra in your EPF!

So you see, it is really difficult to NOT have enough in the EPF. For most people, it is so easy to have too much instead, and one thing for sure, Malaysia will have too many people retiring with more than half a million in their EPF within the next few years, the numbers will greatly surprise you when it is revealed (why don’t the EPF reveal it now using projections?)

Our discussion will not be complete without a discussion on the expenses part of a retiree. According to established poverty rate for the country, someone who is earning less than RM800 is considered to be one. So everyone is jumping on this statistic, including the EPF, saying a retiree who withdraws RM800 a month and considered to be in “poverty”, will consume his retirement savings in no time (I disagree the retiree will be in poverty due to a wrong benchmark). So let’s calculate!

An average retiree, with RM196,000, deposited his money into ASB after withdrawing it from the EPF, (ASB return of say 7.5% a year, facing an inflation of 3% a year). The retiree withdraw RM800 a month from his retirement fund. How long his retirement money would last?

Forever.

Yes, the money would not run out, it will just keep on growing and growing, until he dies. By the time he is 85 years old, it would have grown to RM646,000. This is despite that he is withdrawing the money at RM800, every month, with inflation taken into account (at the age of 85, he will withdraw RM1,885 a month due to inflation). Still, the money would continue to grow unabated. What retirement crisis are they harping about??

The retiree can actually withdraw RM1,300 a month, for a really comfortable life during retirement, and finish up all of his money by his 85th birthday (or “death day” unfortunately).

But then, how about those who have less than RM196,000 upon retirement? Well, for your information, there is a problem with the poverty calculation of RM800 a month. It was not intended for a retiree in the first place. It was intended for a working person having dependents and having to fork money for transport and housing. For a retiree who have minimal transport costs, no dependents (only the significant other is), and a fully paid up house, RM800, a month and for every single month is really is, a lot of money. Use it for eating out? That’s a lot. Use it for travelling? It is more than enough. Of course a retiree will have the occasional RM200 from the children and other incomes which they usually get by working part time (don’t forget BR1M!). In short, a retiree will be able to retire comfortably at perhaps RM550 a month for food and the usual expenses.

So I hope everyone will not get confused and simply apply the poverty rate onto our would-be retirees. They are not the same as working adult anymore. Retirees in their 60s will no longer have any school going children, won’t be having any housing loan left (unless they borrow beyond their capabilities). Their overhead is small compared to let say a father of 5 growing children, with house and a car loan!

Apart from that, retirees have their fully paid up properties in their disposal. In some countries, reverse mortgages are available, enabling access to a locked up assets. Thinking about it, why should you leave your property behind for someone else? You should make full use of it, and consumed it in totality. Leave it to the children? Why? As a retiree, if your children are living with you in your very own house, do charge them rent and your income would have increase, easily. And that is fair. Another option is to downsize by selling the house and move into a smaller but a cheaper home, freeing cash for daily expenses. Yet another simple option is to simply sell and then rent.

I don’t see any retirement crisis looming upon the horizon. The only crisis I can see is the lack of education for Malaysians in managing their money. The government cannot hold their hands like a child until death. A retiree should have learned by then on managing their own money. If they couldn’t, it is obvious that the education system is to be blamed. We cannot let a few bad apples to affect the entire group of retirees. We cannot create rules to affect everyone due to just a few bad apples. There are many retirees who are actually prudent with their money. The EPF should pay these retirees to teach other retirees, it will bring more value. Even the EPF needs to be well versed with its data and its contributors and stop scaring its contributors.

There is actually a different kind of crisis happening out there. Malaysian workers have money, and at the moment when they really need it most, they could not use it as it is stuck in the EPF. They could then miss on out many wonderful opportunities, sticking onto their jobs and delaying their dreams. This is plain bad for the economy. Some may become bankrupt, and completely ruin their lives. And when they don’t need any more money to cover for expenses, then the tucked away EPF money would come, and it would come in a gush. The crisis would be, a crisis of waste; it will be simply wasted, not on dreams and other efficiency improvements, but on pent up consumption of silly things. Already, there are many retirees remarry upon receiving their EPF dues, some just spend their money to no end, buying fancy cars they don’t even need, and many other wasteful ventures including getting ‘scammed’ by a growing bunch of vampires. This hypothetical situation is just not good for the economy.

A retiree can choose to adjust his expenses, so that his money would last. He also can choose to work part time, to make the money really last. In short, a retiree is not without options upon retirement, even with only an average or below average retirement savings.

The EPF must show and reveal the data for those who work and contribute their entire lives, what their typical EPF balance would be. For those who choose to work only part time, they should not be the main focus of the EPF. Even for active contributors, they must be filtered out and only those who contributed in excess of 25 years are to be counted.

Many workers and would-be retirees, have additional assets other than their EPF. For some of them, they have much more in their properties, businesses and other ventures and assets, than their EPF savings. Thus the EPF simple conclusion that retirees do not have enough is just shady statistics without the full data revealed and analyzed. EPF must make thorough calculations and reveal the raw data to us to check it.

If the EPF want a faster increase in Malaysians’ EPF balances, why don’t the EPF ask its contributors to stop smoking? It sure beat any proposal out there, there is no need to increase contribution or withdrawal age, or to burden our companies further (by raising their contribution percentage until they aren’t competitive). By stopping the habit of smoking, smokers would have an extra RM459,000 in their account upon retirement. Just think about it, more than 40% of Malaysians are smokers (depending on the age group). And to those who smoke regularly, don’t ever complain about not having enough money for retirement. It is solely your own fault, and has nothing to do with the EPF, the government or anyone else. Smoking is never good for economy, society or health!

In my view, we must invest and focus more on education. Financial management and efficiency improvements are important factors for each of us. The EPF must put a stop to its arbitrary adjustments to contributors’ rights such as the withdrawal age and other limits. The EPF must stop its practice of scaring the Malaysian people. Please, publish and release your raw data, and let us judge whether your imagined retirement crisis would warrant an adjustment to the EPF Act.

Luckily, the Prime Minister has quickly stepped in, and joined the debate, but not to prolong it, but to end it for good. Not under my watch! That is the clear proclamation made by the PM. [Sometimes I wonder why the PM declined to act for the extremists’ view of some of our Muslims counterparts in the country]. It is clear that our PM do not want the withdrawal age increase to happen under his term and to be forever branded and eternally remembered as the person who made the most unpopular of decisions. Many still vividly remember one of the assurances made by the PM during the many speeches during the debate to increase the retirement age to 60 years old; one is which that the withdrawal age for the EPF shall not be changed. Fortunately for us, the PM remembers! I guess the EPF will have to wait for the next prime minister of Malaysia to be in office before it presses for a change, and until then, Malaysians can sleep easy knowing their access to the contributed money would not be changed.

The EPF must take note that not everyone in Malaysia intends to retire at the age of 60, and increasing the withdrawal age is a cruel act of robbing our money from us. Stop using the existing retirement age as a reason to impose higher withdrawal age. The retirement age is simply a law that allows the people to continue to work in their existing and official capacity up to 60 years of age. Even this law permits anyone to retire as and when they choose. We don’t have to work until 60 years of age! It is never mandatory. So why can’t the EPF follow suit and allows its contributors’ a decent retirement age of their choosing?

The author or this article can be reached via his website at http://sirikegagalanemas.wordpress.com and his books, including a free away book, can be sighted in Google Play. Sharif Rahman also is the co-author of the 259 Trillion Vs 5 Trillion series which can be obtained from Amazon.